Mortgage Rates Average 6.51%

May 21, 2026

The 30-year fixed-rate mortgage averaged 6.51% this week. As rates fluctuate, aspiring buyers should remember that by shopping around for the best mortgage rate and getting multiple quotes, they can potentially save thousands.

- The 30-year fixed-rate mortgage averaged 6.51% as of May 21, 2026, up from last week when it averaged 6.36%. A year ago at this time, the 30-year FRM averaged 6.86%.

- The 15-year fixed-rate mortgage averaged 5.85%, up from last week when it averaged 5.71%. A year ago at this time, the 15-year FRM averaged 6.01%.

Information provided by Freddie Mac.

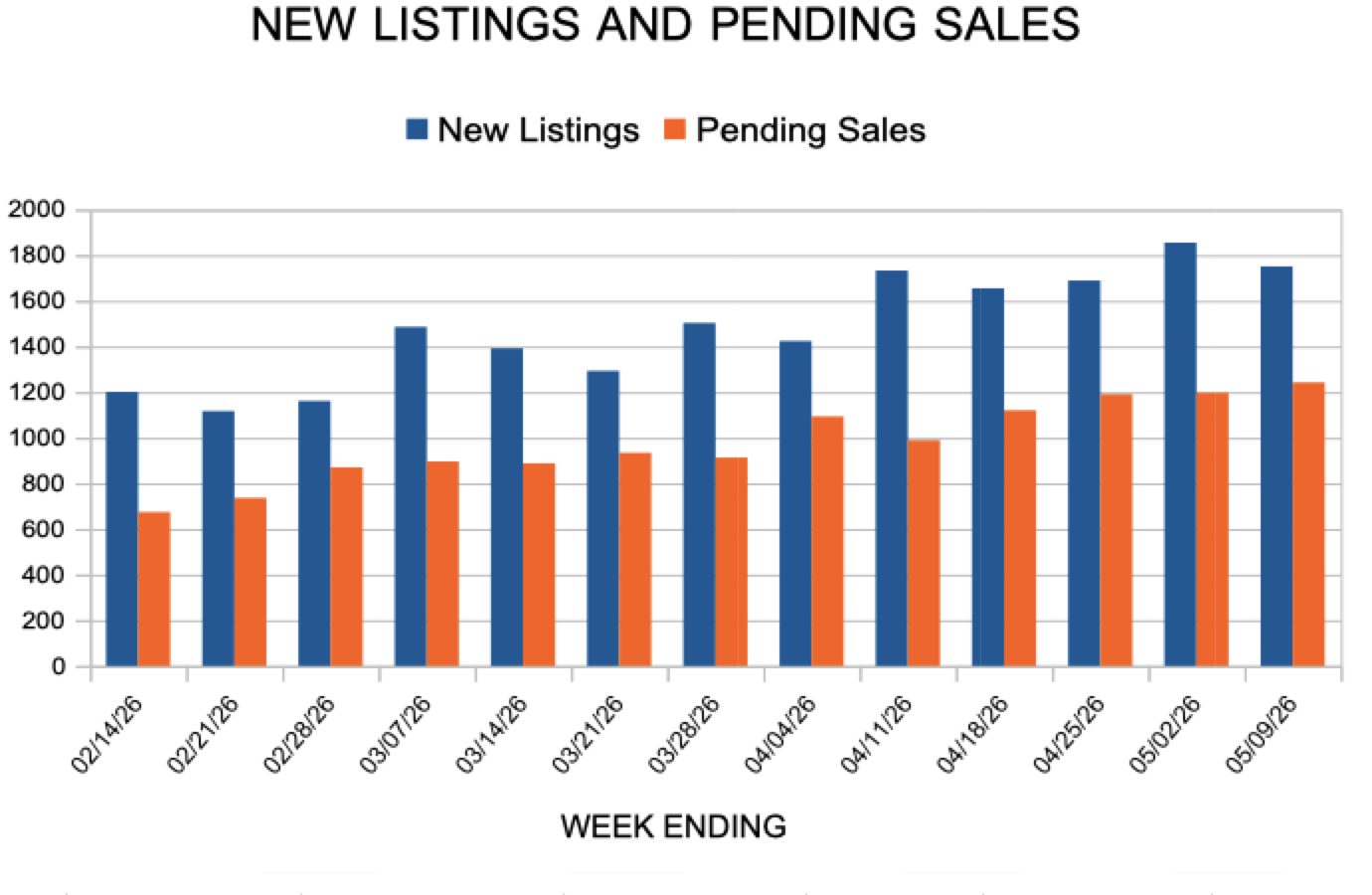

New Listings and Pending Sales

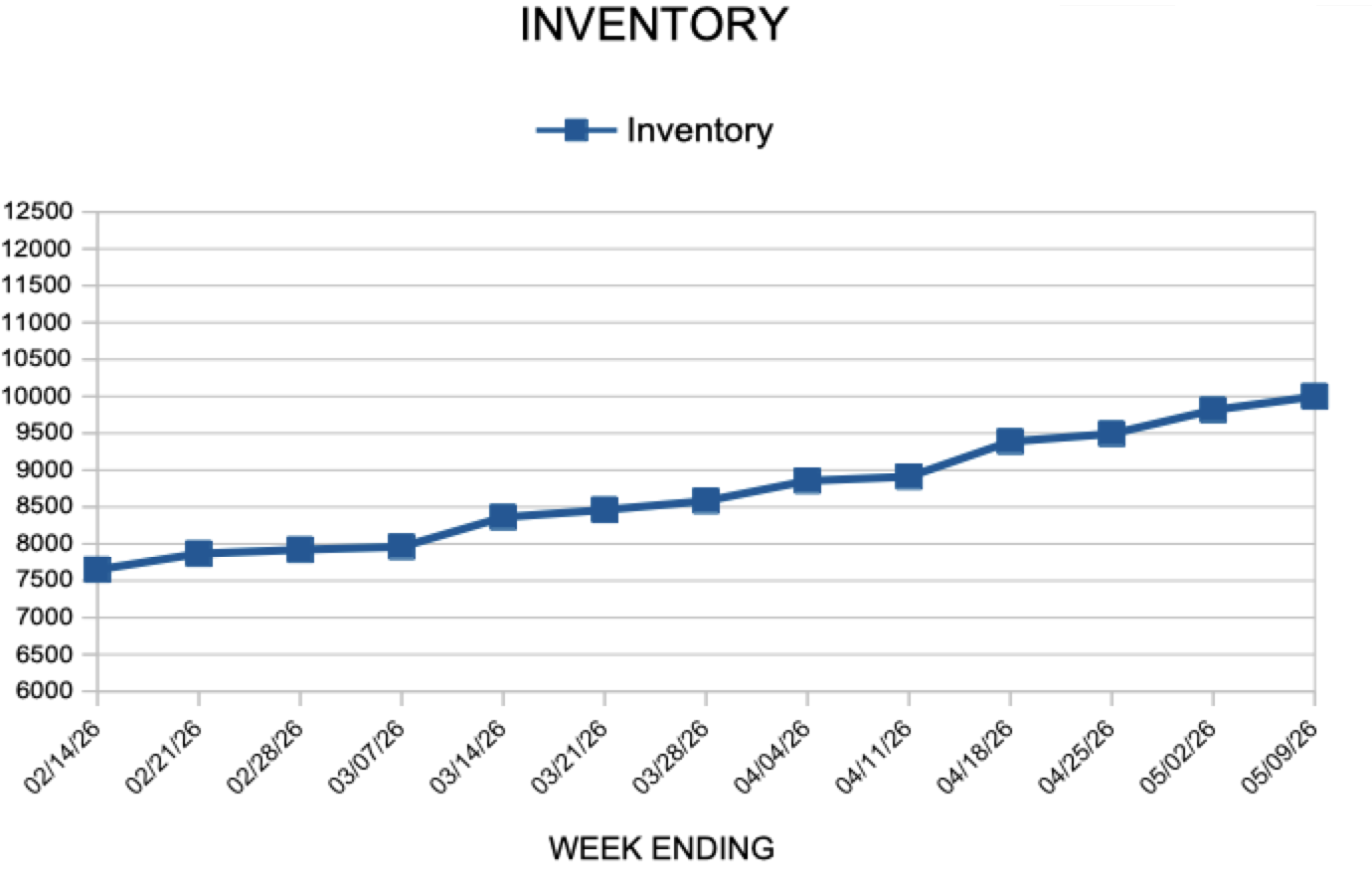

Inventory

Weekly Market Report

For Week Ending May 9, 2026

2026 has been the strongest spring for new listings since 2022, with listing activity up 8.7% month-over-month and 1.1% year-over-year in April, according to Realtor®.com. Among major metropolitan areas, Virginia Beach had the strongest new listing growth at 23.8% year-over-year, followed by Indianapolis at 21.1% and Louisville at 19.2%.

In the Twin Cities region, for the week ending May 9:

- New Listings increased 4.5% to 1,751

- Pending Sales increased 14.2% to 1,242

- Inventory increased 8.9% to 9,999

For the month of April:

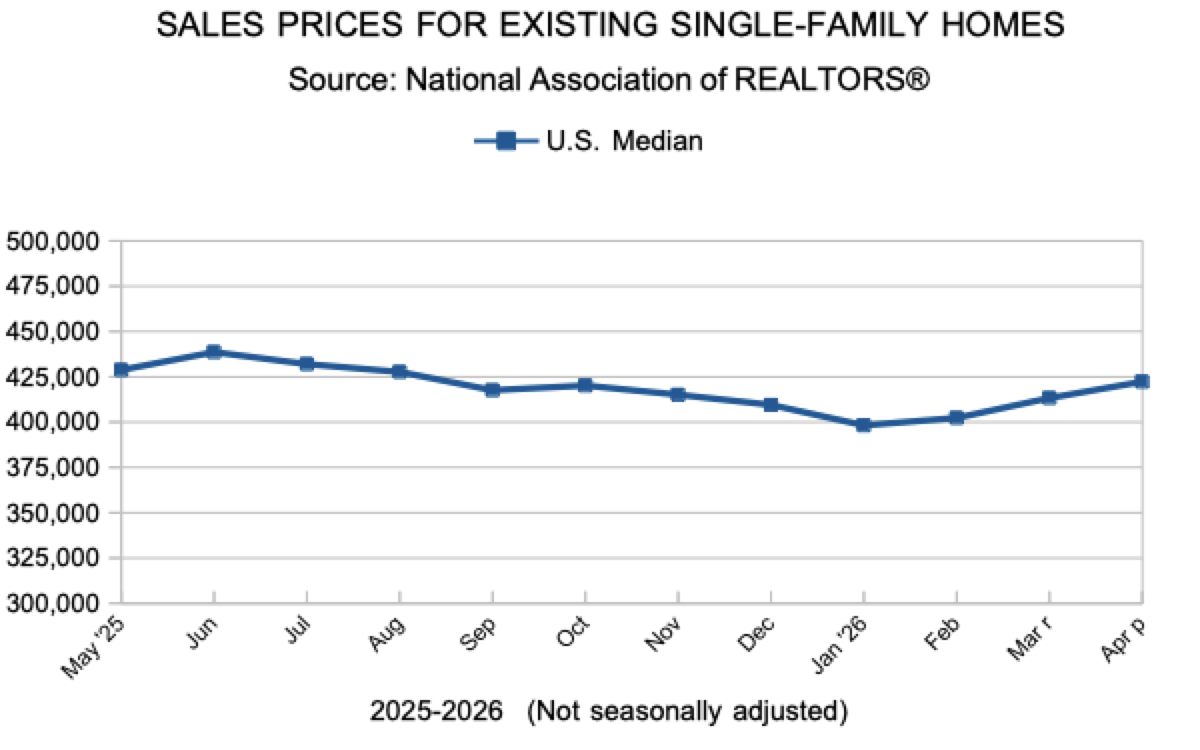

- Median Sales Price decreased 2.0% to $392,000

- Days on Market increased 14.0% to 57

- Percent of Original List Price Received decreased 0.4% to 99.3%

- Months Supply of Homes For Sale increased 8.3% to 2.6

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.