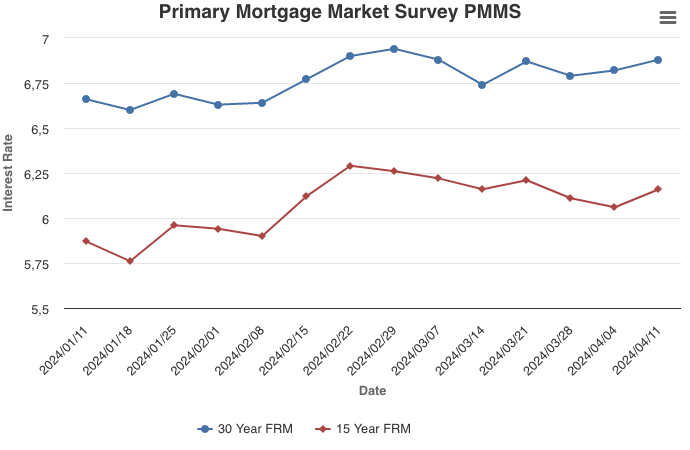

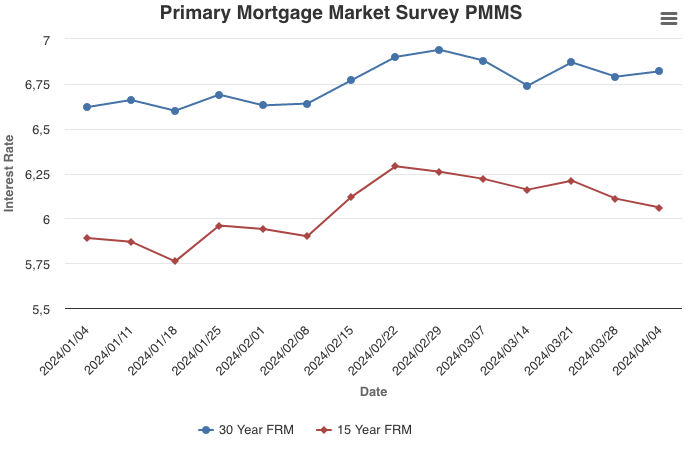

For Week Ending April 6, 2024

For Week Ending April 6, 2024

The share of homebuyers who paid cash for their home reached a 10-year high recently, according to the National Association of REALTORS®, with cash buyers accounting for 32% of all home purchases in January. Real estate investors and vacation-home buyers made up the majority of cash buyers during the past 6 months; among those consumers who paid cash for a home purchase last year, 26% were repeat buyers, while just 6% were first-time buyers.

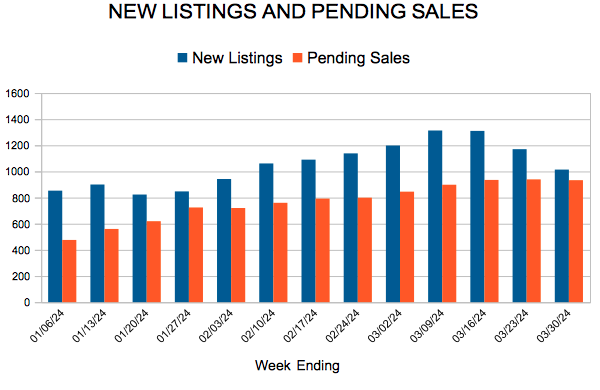

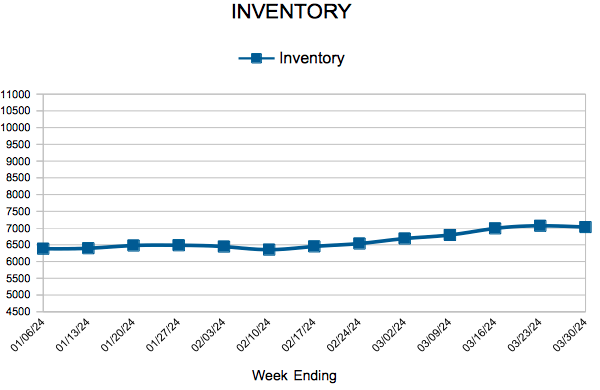

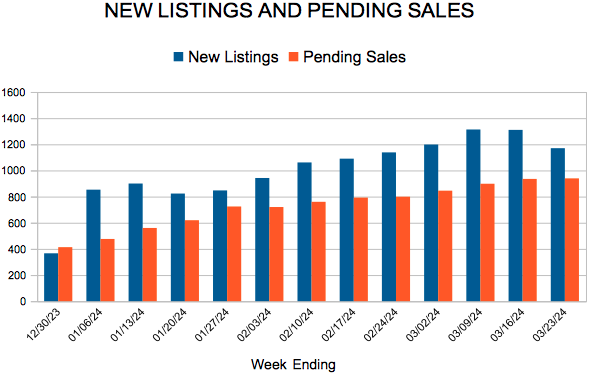

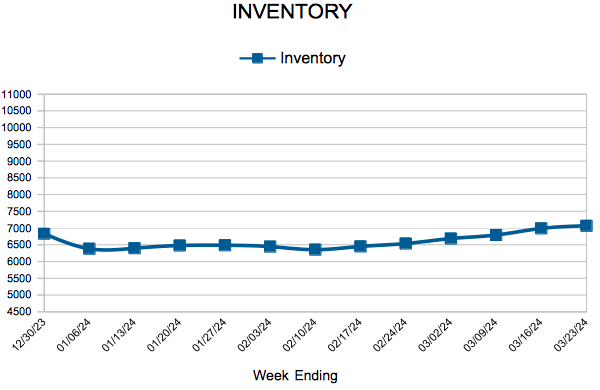

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING APRIL 6:

- New Listings increased 32.2% to 1,383

- Pending Sales decreased 0.7% to 892

- Inventory increased 13.4% to 7,048

FOR THE MONTH OF FEBRUARY:

- Median Sales Price increased 4.6% to $358,000

- Days on Market decreased 3.3% to 59

- Percent of Original List Price Received increased 0.3% to 97.5%

- Months Supply of Homes For Sale increased 35.7% to 1.9

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.