New Listings and Pending Sales

A new report from Realtor®.com found that new construction homes are more likely to sell below list price than existing homes. Condos and townhomes are also more likely to sell below list price than single-family homes. As of March 2026, the average single-family home sold for 99.2% of its final list price, while the average condo sold for 97.9% of its final list price.

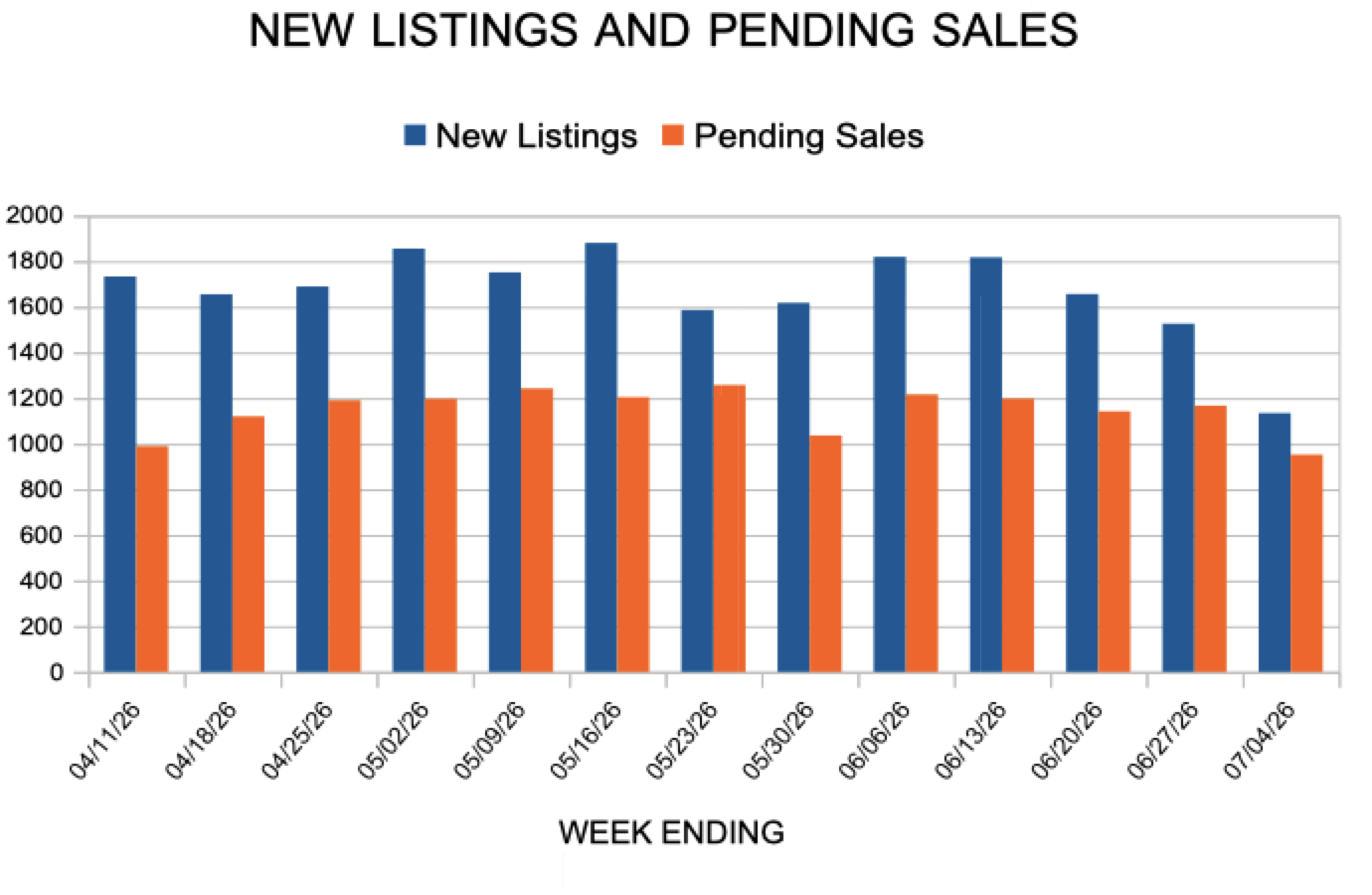

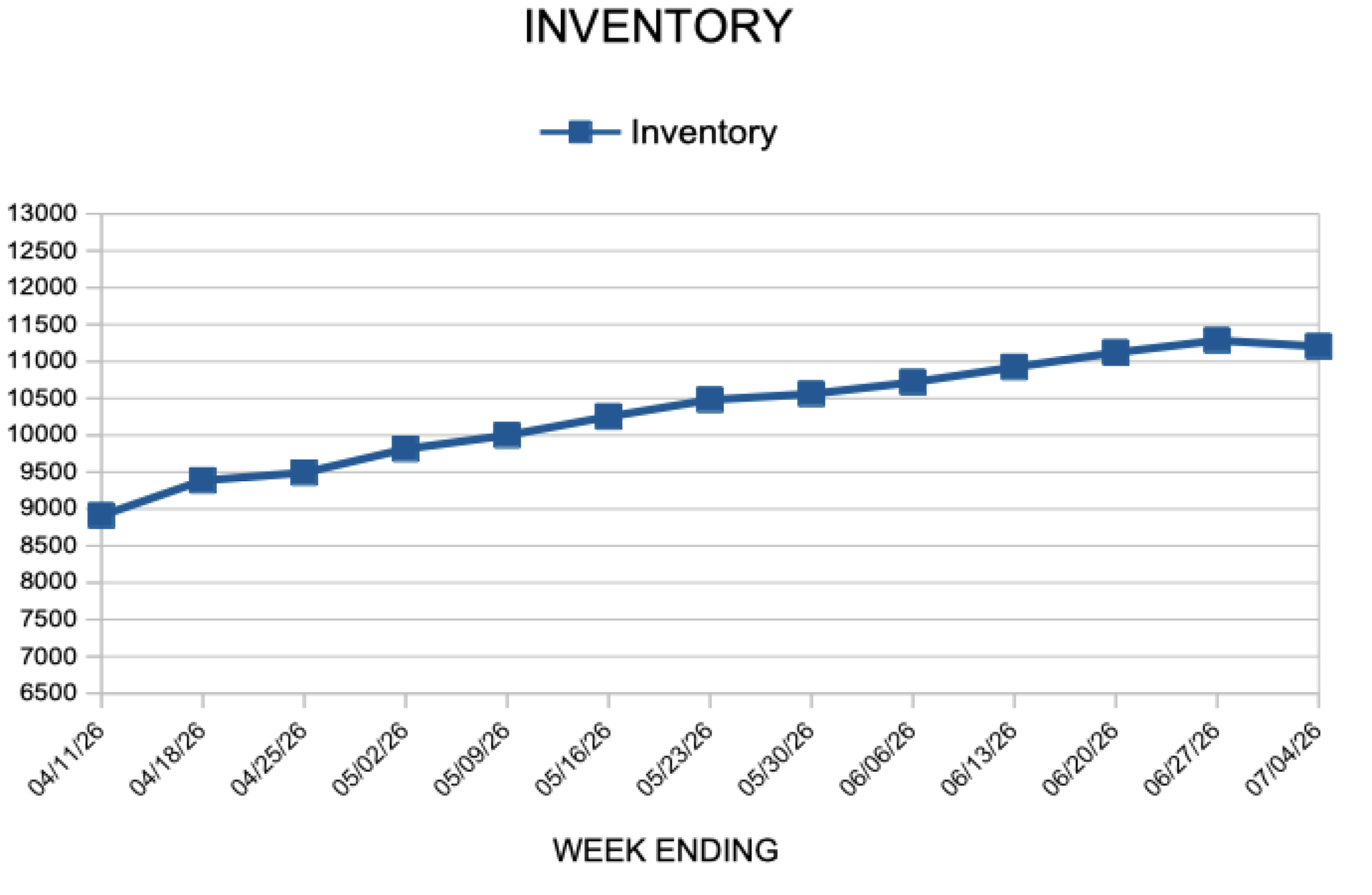

In the Twin Cities region, for the week ending July 4:

For the month of May:

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

The 30-year fixed-rate mortgage averaged 6.49% this week. Mortgage rates have not changed much recently, but economic growth and housing affordability continue to improve for homebuyers as they shop for homes in today’s market.

Information provided by Freddie Mac.

Realtor®.com found that buying a home by age 30 is associated with a 22.5% higher net worth at age 50 compared with purchasing a first home in one’s 40s. Moreover, children raised in homeowner households are 18.4% more likely to become homeowners by age 35. The U.S. homeownership rate stood at 65.7% in the fourth quarter of 2025, the highest level of the year, though still below the pandemic-era high of 67.9% in the second quarter of 2020.

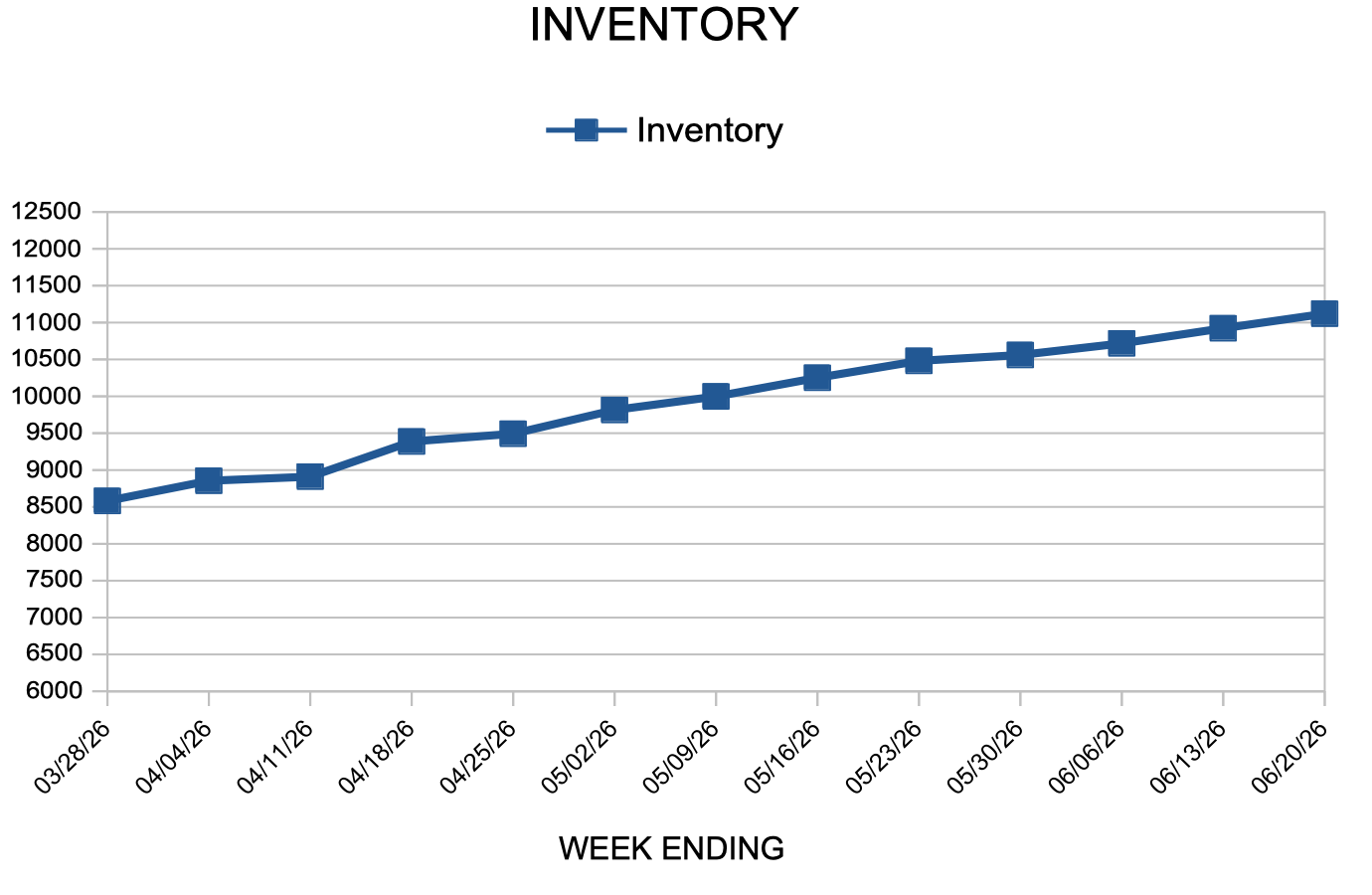

In the Twin Cities region, for the week ending June 27:

For the month of May:

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

The 30-year fixed-rate mortgage eased slightly this week averaging 6.43%. With rates at a seven-week low and purchase demand continuing to edge higher, it’s an encouraging sign as prospective homebuyers respond to modest improvements in affordability.

Information provided by Freddie Mac.