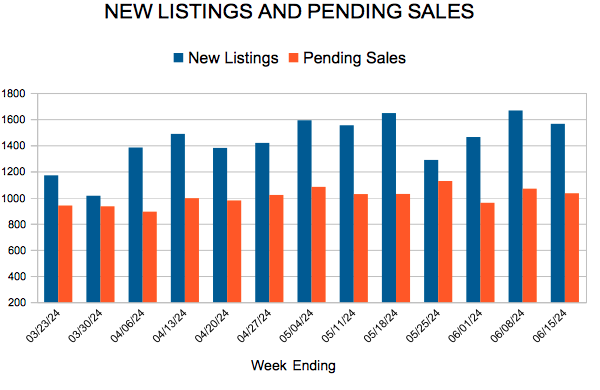

New Listings and Pending Sales

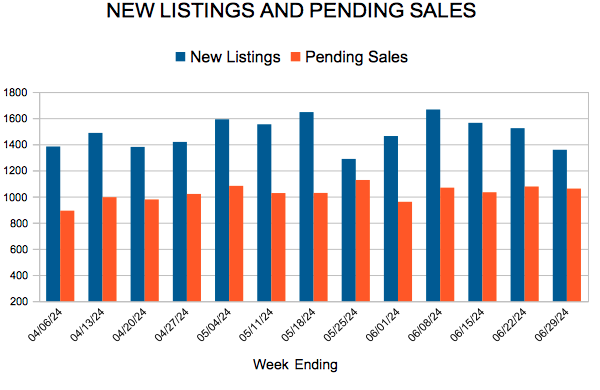

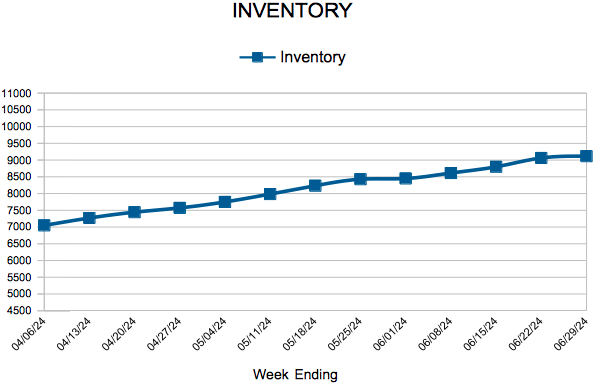

For Week Ending June 29, 2024

For Week Ending June 29, 2024

Nationally, the median down payment was $26,400, or 13.6% of the purchase price, in the first quarter of 2024, according to a recent study from Realtor.com, a slight decrease from the previous quarter, when the median down payment was $30,400 (14.7%). Down payments are up significantly from pre-pandemic levels: in the first quarter of 2020, the typical down payment was approximately $14,000, or 10.7% of the purchase price.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JUNE 29:

FOR THE MONTH OF MAY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

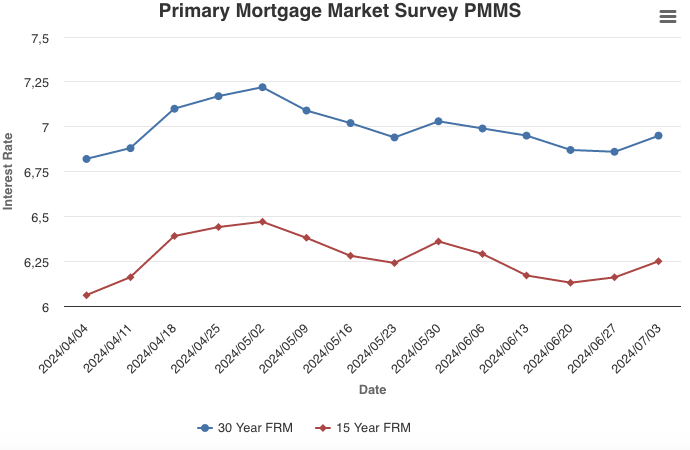

July 3, 2024

Mortgage rates increased this week, coming in just under seven percent. Both new home and pending home sales are down, causing active listings to rise. We are still expecting rates to moderately decrease in the second half of the year and given additional inventory, price growth should temper, boding well for interested homebuyers.

Information provided by Freddie Mac.

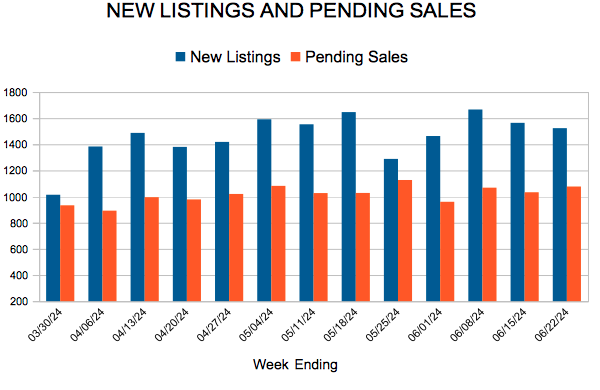

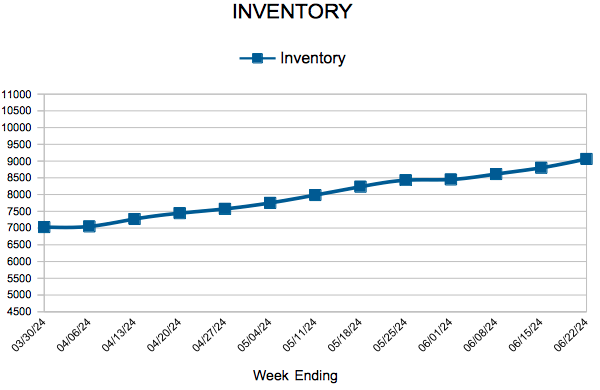

For Week Ending June 22, 2024

For Week Ending June 22, 2024

The number of homes for sale continues to increase nationwide, with Realtor.com reporting there were 35.2% more homes for sale on a typical day in May compared to the same time last year, marking the seventh consecutive month of annual inventory growth. In fact, from January through May, inventory was at its highest level since 2020, although it is still down considerably from normal 2017 – 2019 levels.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JUNE 22:

FOR THE MONTH OF MAY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

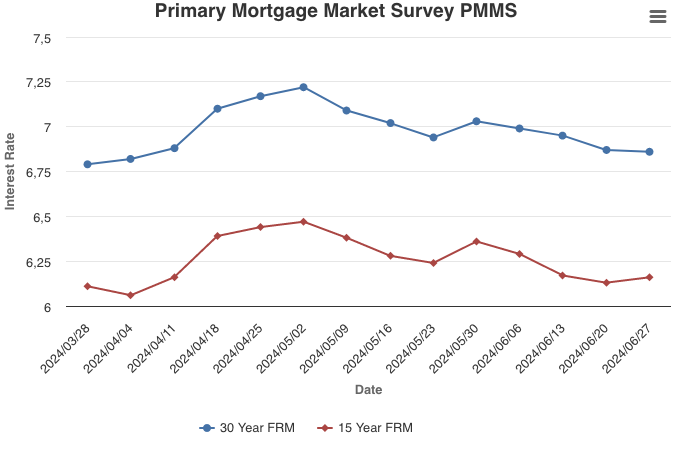

June 27, 2024

The 30-year fixed-rate mortgage continues to trend down, hitting the lowest level in almost three months. By historical standards, the economy is in good shape, and we expect rates to continue to come down over the summer months, bringing additional homebuyers back into the market.

Information provided by Freddie Mac.

Licensed In Minnesota

All information deemed reliable but not guaranteed and should be independently verified.