Inventory

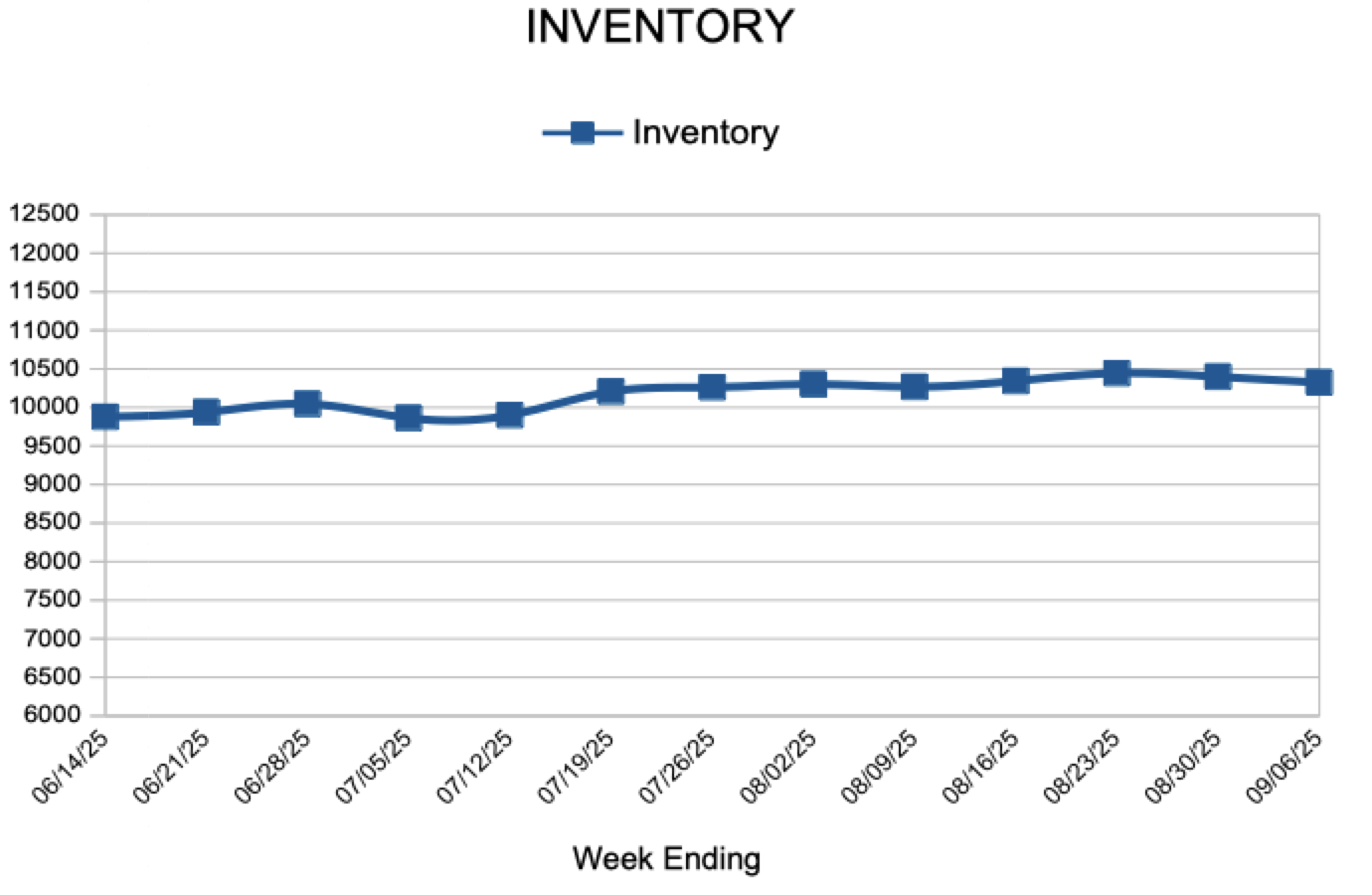

For Week Ending September 6, 2025

For Week Ending September 6, 2025

U.S. housing starts rose to a five-month high, climbing 5.2% month-over-month and 12.9% year-over-year to a seasonally adjusted annual rate of 1,428,000 units, according to the U.S. Census Bureau. The gain was driven primarily by multi-family starts, which surged 11.6% from the previous month to 470,000 units, while single family starts increased 2.8% to 939,000 units.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING SEPTEMBER 6:

FOR THE MONTH OF AUGUST:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

September 11, 2025

The 30-year fixed-rate mortgage fell 15 basis points from last week, the largest weekly drop in the past year. Mortgage rates are headed in the right direction and homebuyers have noticed, as purchase applications reached the highest year-over-year growth rate in more than four years.

Information provided by Freddie Mac.

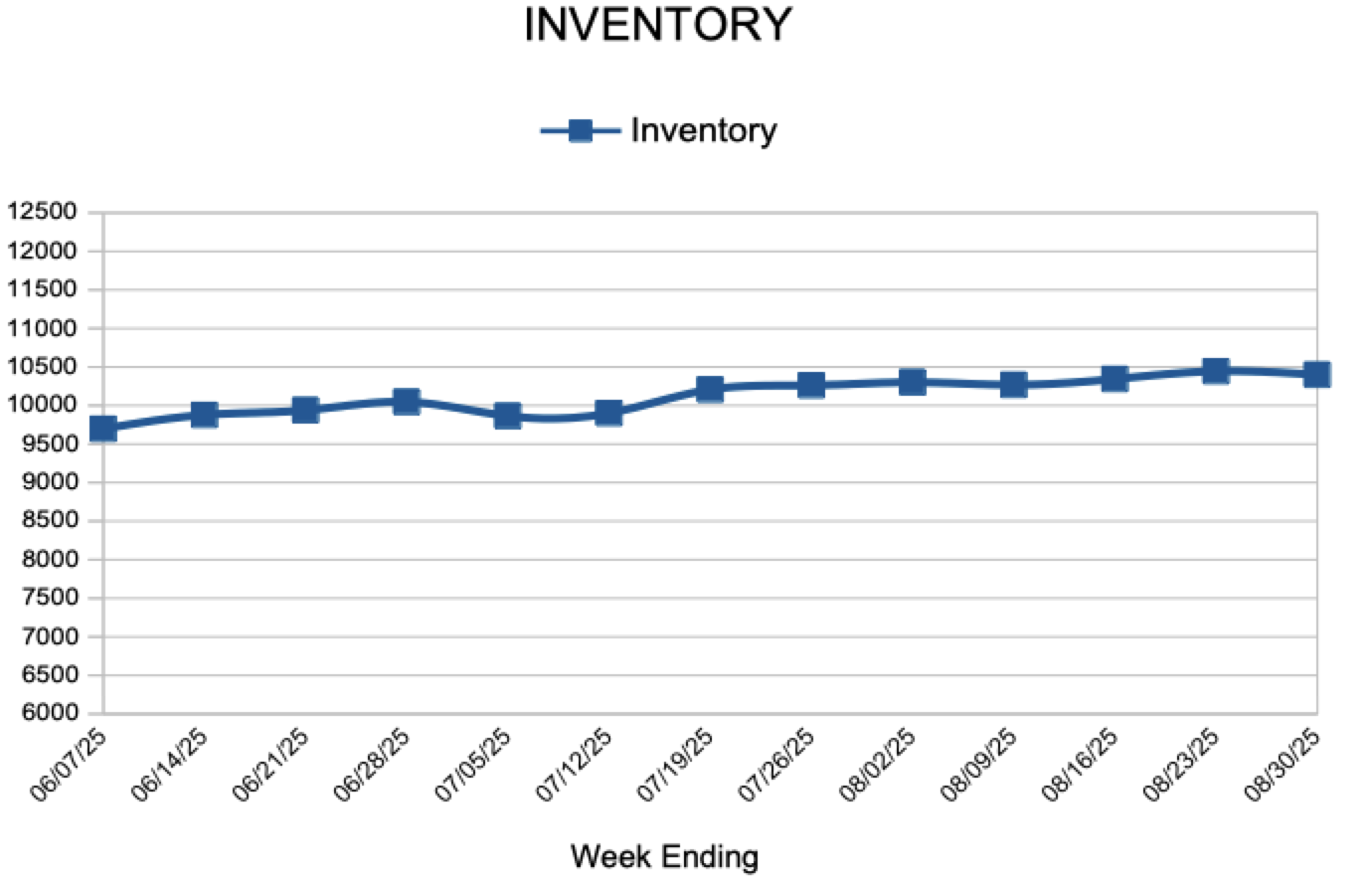

For Week Ending August 30, 2025

For Week Ending August 30, 2025

Investors purchased 265,000 homes—nearly 27% of all homes sold—in the first quarter of 2025, according to a recent report from BatchData. That’s a 1.2% increase from the same period last year and represents the highest share in at least five years. Between 2020 and 2023, investors purchased an average of 18.5% of homes sold. Investor-owned properties now account for approximately 20% of the country’s 86 million single-family homes.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING AUGUST 30:

FOR THE MONTH OF JULY:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

September 4, 2025

Mortgage rates continue to trend down, increasing optimism for new buyers and current owners alike. As rates continue to drop, the number of homeowners who have the opportunity to refinance is expanding. In fact, the share of market mortgage applications that were for a refinance reached nearly 47%, the highest since October.

Information provided by Freddie Mac.

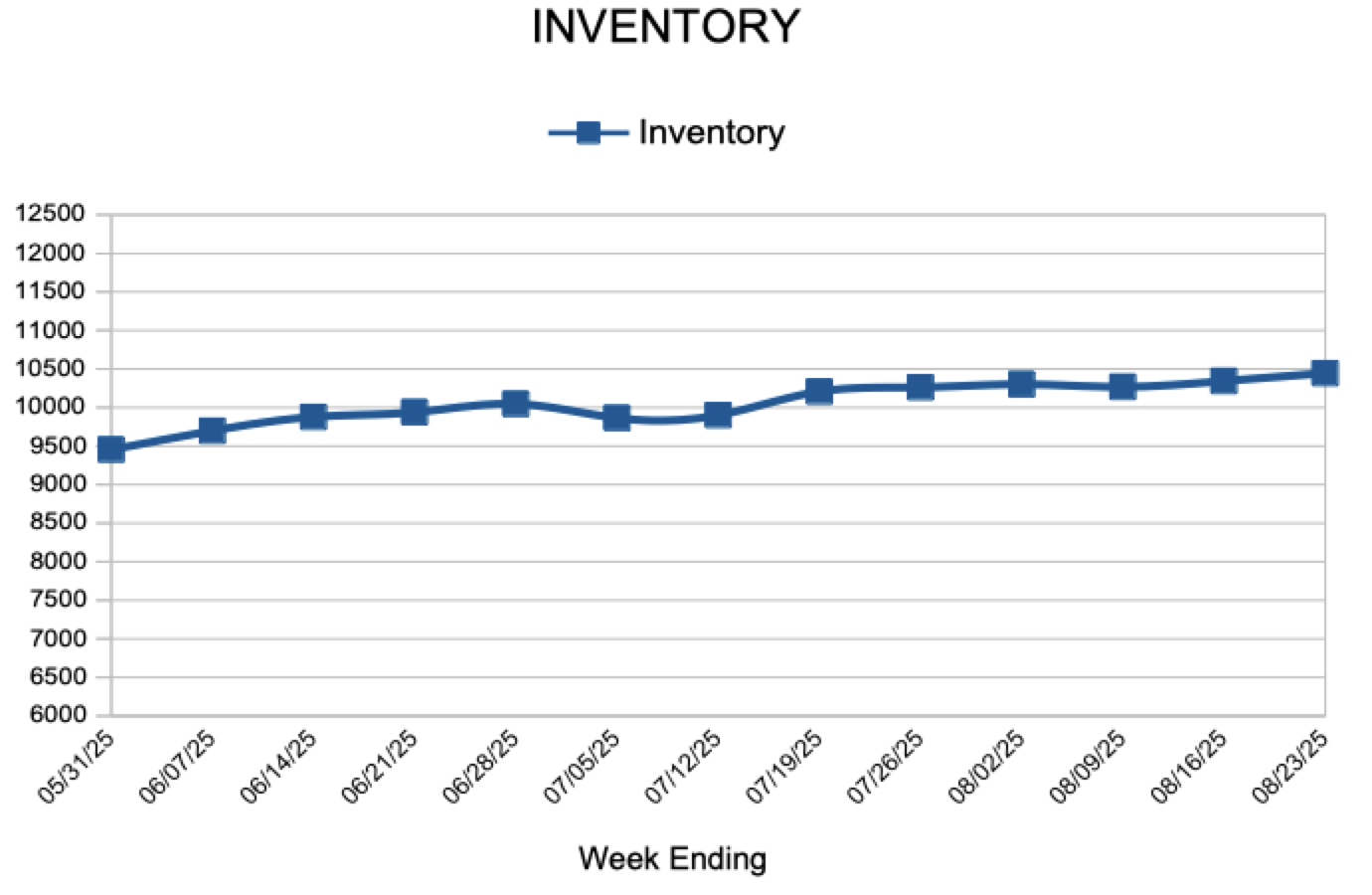

For Week Ending August 23, 2025

For Week Ending August 23, 2025

According to Realtor®.com’s July 2025 Monthly Housing Market Trends Report, national housing inventory increased 24.8% year-over-year, with more than 1.1 million homes for sale in July. This marks the third consecutive month with over 1 million active listings. While this is encouraging news for buyers, total active listings remain 13.4% below typical 2017-2019 levels.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING AUGUST 23:

FOR THE MONTH OF JULY:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

Licensed In Minnesota

All information deemed reliable but not guaranteed and should be independently verified.