New Listings and Pending Sales

For Week Ending July 22, 2023

For Week Ending July 22, 2023

Home prices hit a new high in May, rising a seasonally adjusted 0.7% month-overmonth, according to the latest Black Knight Home Price Index (HPI), marking the fifth consecutive monthly price increase. The report found that 27 of the 50 largest markets have seen prices return to or exceed their 2022 peaks, with many of those markets located in the Midwest and Northeast, although price gains remain weaker in the West and in areas that saw significant price gains during the pandemic.

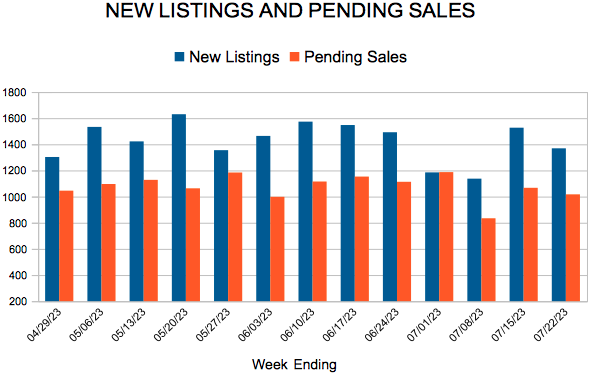

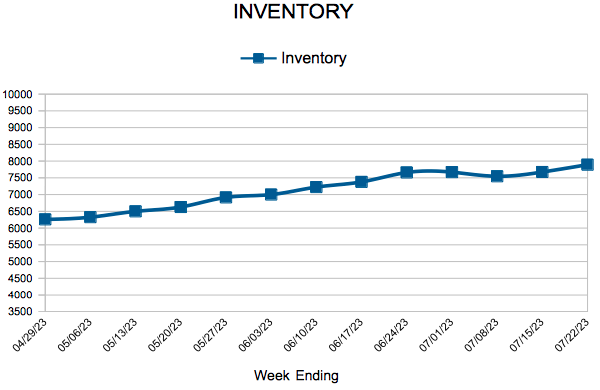

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JULY 22:

FOR THE MONTH OF JUNE:

All comparisons are to 2022

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

July 20, 2023

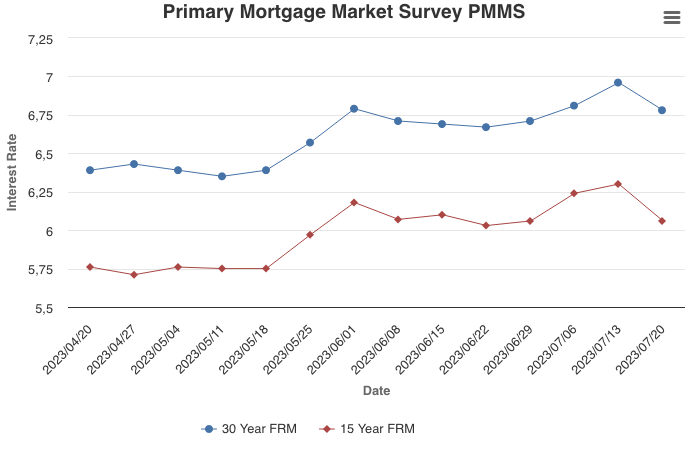

As inflation slows, mortgage rates decreased this week. Still, the ongoing shortage of previously owned homes for sale has been a detriment to homebuyers looking to take advantage of declining rates. On the other hand, homebuilders have an edge in today’s market, and incoming data shows that homebuilder sentiment continues to rise.

Information provided by Freddie Mac.

(July 16, 2023) – According to new data from Minneapolis Area REALTORS® and the Saint Paul Area Association of REALTORS®, home prices rose slightly in June. Both buyer and seller activity were also lower compared to last June.

Sales & Prices

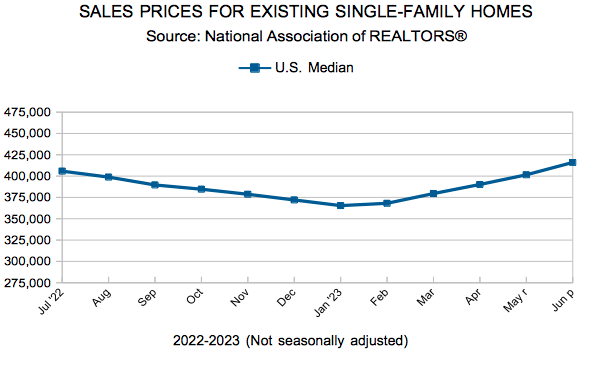

Prices were down slightly in April and May but up 0.5 percent in June. April marked the first year-over-year price decline since February 2012. Half of all homes sold for over $382,000. But as in April and May, sellers in June still accepted offers above list price despite a decline in sales—a dynamic that reflects the lack of supply despite rising mortgage rates. Sellers received offers at 101.3 percent of their asking price. Market times—while up—still reflect a relatively fast-paced market. Half the sales went under contract in under 12 days. And homes are still selling faster than in June 2018, 2019 and 2020.

“Some remain convinced of an impending crash, but we’re still not seeing it,” said Brianne Lawrence, President of the Saint Paul Area Association of REALTORS®. “Two months of prices softening around 1.0 percent before climbing again is more like a blip or pause than a downturn.” But the Fed-driven decline in demand persists. As we compare to slower months of 2022, the sales declines have moderated. Pending sales dipped 10.8 percent; closed sales fell 18.0 percent.

Listings and Inventory

June sellers brought 16.5 percent fewer new listings to market than last year. Inventory levels slid 9.0 percent lower. Some sellers are choosing to stay put and wait instead of selling for a lower price. Most sellers are also buyers and are reluctant to trade away their 3.0 percent interest rate for 6.8 percent. “Even with fewer sales in light of higher rates, homes are still selling relatively quickly while sellers get relatively strong offers,” said Jerry Moscowitz, President of Minneapolis Area REALTORS®. “That’s partly driven by homeowners with rates under 4.0 percent staying put.”

Both supply and demand have come down in tandem, meaning the balance between buyer and seller activity has remained tight. Inventory levels fell 13.4 percent in June to 7,492 active listings. The market still favors sellers, but not to the same degree as the last few years. Our 2.0 months supply of inventory was up 17.6 percent. Typically 4-6 months of supply are needed to achieve a balanced market.

Location & Property Type

Market activity varies by area, price point and property type. New home sales rose 24.3 percent while existing home sales were down 12.8 percent. Single family sales fell 13.7 percent, condo sales declined 3.2 percent and townhome sales were up 0.8 percent. Sales in Minneapolis decreased 12.1 percent while Saint Paul sales fell 12.9 percent. Cities such as Annandale, Shorewood, White Bear Township and Delano saw the largest sales gains while White Bear Lake, New Hope, New Prague, Zimmerman and Hudson all had notably lower demand than last year.

June 2023 Housing Takeaways (compared to a year ago)

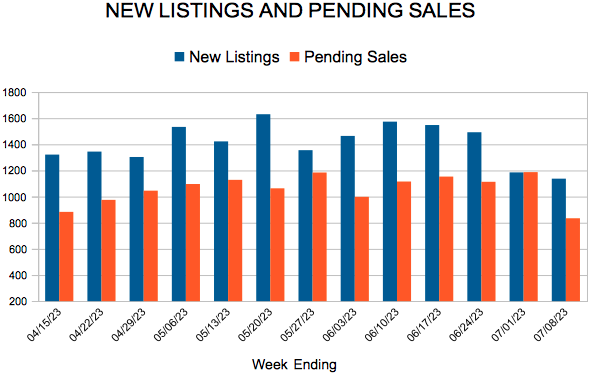

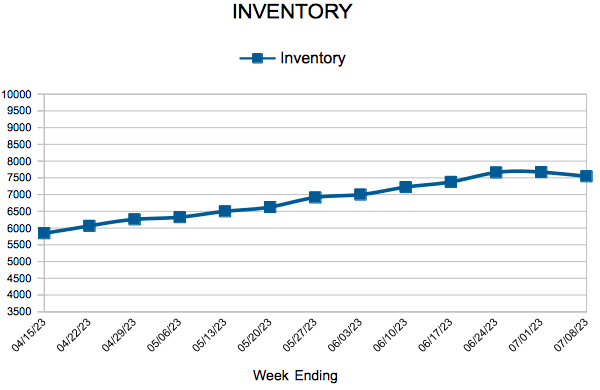

For Week Ending July 8, 2023

Rental prices are beginning to decline, with rents for 0-2 bedroom properties dropping 0.5% year-over-year to $1,739 per month among the 50 largest metropolitan areas, according to Realtor.com’s most recent Monthly Rental Report, marking the first annual decline since 2020, when trend data began. Despite the nationwide decline, rents continue to rise in more affordable areas such as the Midwest and the Northeast, where demand has remained especially strong due to robust job markets and limited rental inventory.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JULY 8:

FOR THE MONTH OF MAY:

All comparisons are to 2022

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

Licensed In Minnesota

All information deemed reliable but not guaranteed and should be independently verified.