Inventory

Realtor®.com found that buying a home by age 30 is associated with a 22.5% higher net worth at age 50 compared with purchasing a first home in one’s 40s. Moreover, children raised in homeowner households are 18.4% more likely to become homeowners by age 35. The U.S. homeownership rate stood at 65.7% in the fourth quarter of 2025, the highest level of the year, though still below the pandemic-era high of 67.9% in the second quarter of 2020.

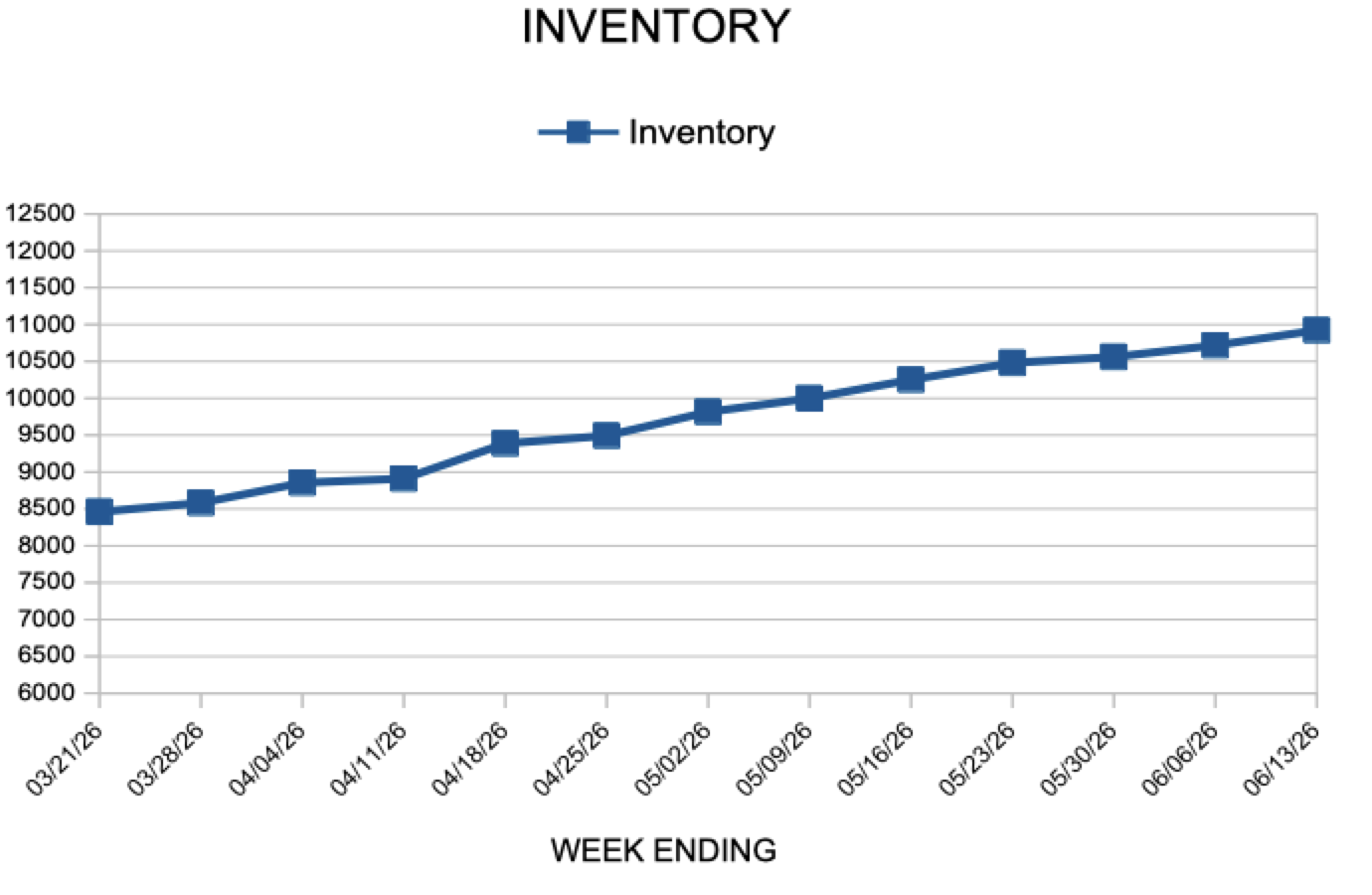

In the Twin Cities region, for the week ending June 27:

For the month of May:

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

The 30-year fixed-rate mortgage eased slightly this week averaging 6.43%. With rates at a seven-week low and purchase demand continuing to edge higher, it’s an encouraging sign as prospective homebuyers respond to modest improvements in affordability.

Information provided by Freddie Mac.

The typical U.S. household spends $39,468 per year on bills, or $3,289 per month, accounting for approximately 47% of annual income, according to doxo’s 2026 U.S. Household Bill Pay Report. Of this total, $24,997 is spent on the 13 most essential household expenses, including housing, utilities, and auto loans. Housing remains the single largest expense category, with mortgage payments totaling $1.08 trillion annually.

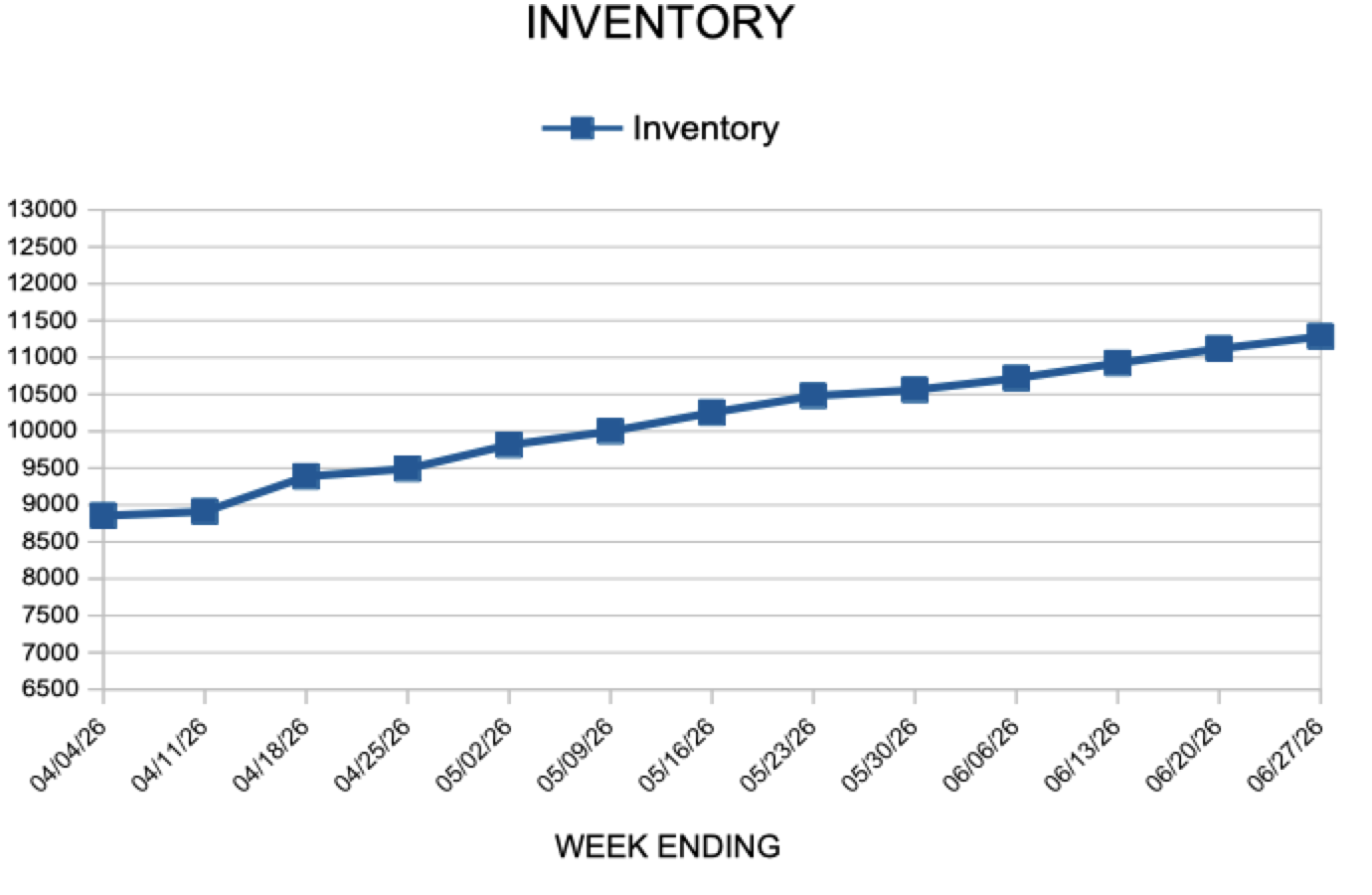

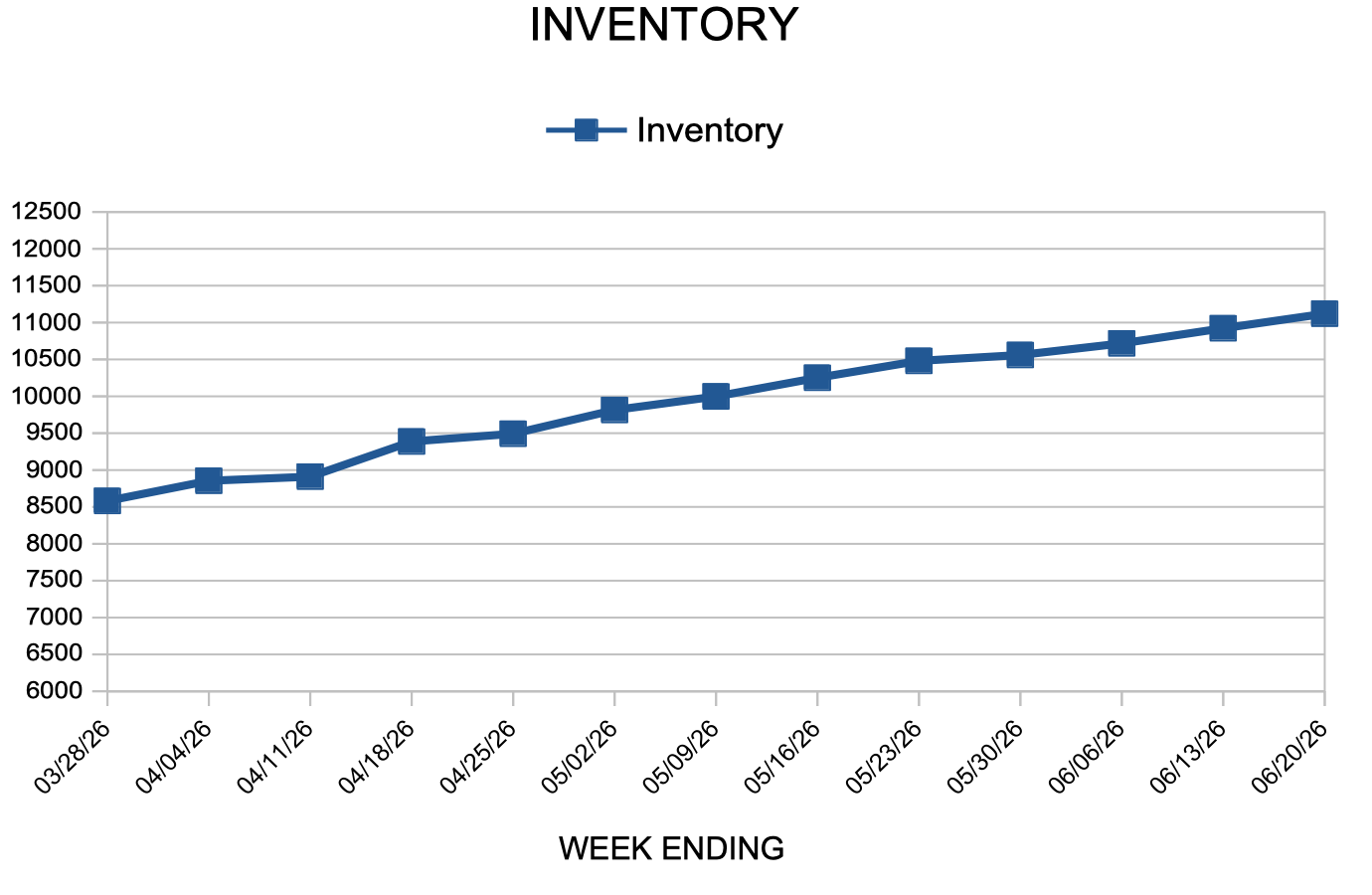

In the Twin Cities region, for the week ending June 20:

For the month of May:

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

The average 30-year fixed mortgage rate was little changed this week at 6.49%. Rates have remained relatively stable over the last six weeks. Meanwhile, purchase activity eased modestly and refinance activity has continued to pick up recently, reflecting borrowers’ responsiveness to current rate levels.

Information provided by Freddie Mac.