For Week Ending January 20, 2024

For Week Ending January 20, 2024

There were 4.9% more homes for sale on the typical day in December compared to the same period in 2022, according to Realtor.com’s December 2023 Monthly Housing Market Trends Report, marking the second consecutive month of annual inventory growth. The number of newly listed homes was also up, rising 9.1% annually, while the total number of unsold homes, including pending listings, was up 3.6% compared to last year.

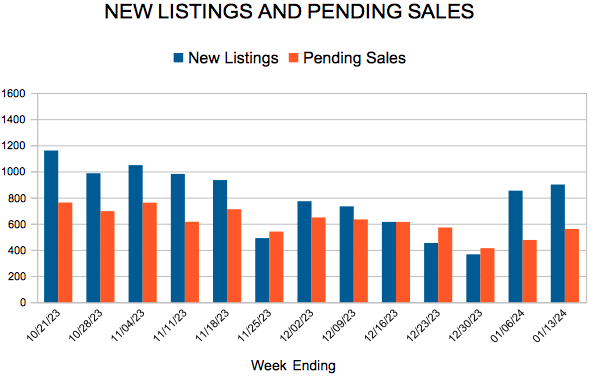

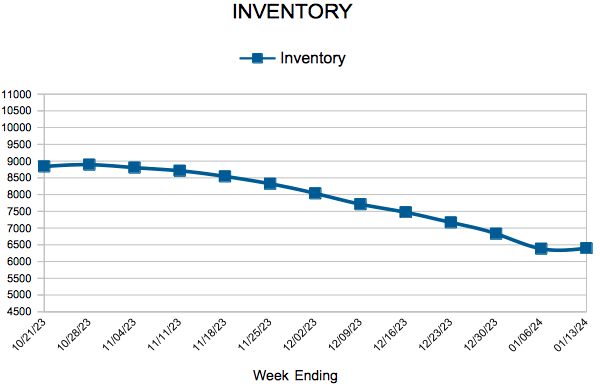

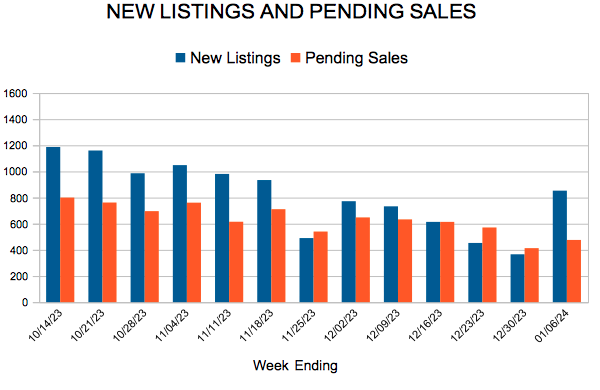

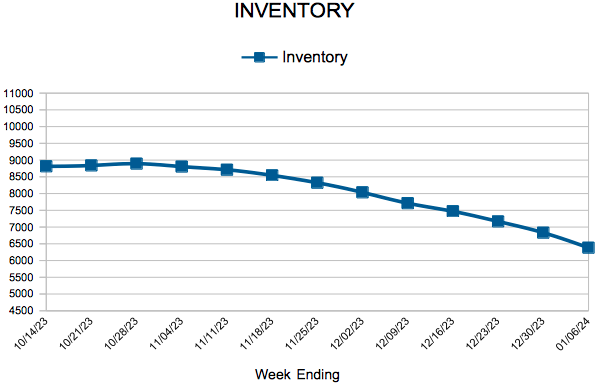

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JANUARY 20:

- New Listings increased 13.8% to 823

- Pending Sales decreased 4.9% to 619

- Inventory decreased 2.3% to 6,478

FOR THE MONTH OF DECEMBER:

- Median Sales Price increased 1.3% to $353,700

- Days on Market remained flat at 50

- Percent of Original List Price Received increased 0.4% to 96.7%

- Months Supply of Homes For Sale increased 13.3% to 1.7

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.