For Week Ending February 17, 2024

For Week Ending February 17, 2024

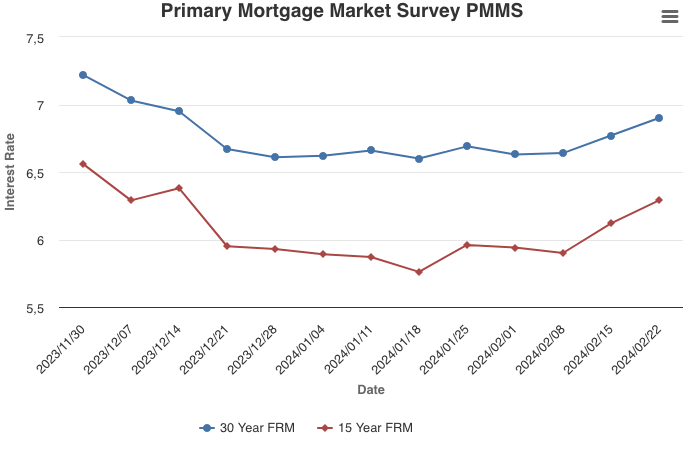

Housing inventory improved for the third month in a row, with the number of homes actively for sale in January increasing 7.9% year-over-year, according to Realtor.com’s January 2024 Monthly Housing Market Trends Report. Lower mortgage rates appear to have brought some sellers back to the market, as the number of newly listed homes rose 2.8% year-over-year. While this is good news for prospective homebuyers, the supply of homes for sale remains down compared to typical 2017 – 2019 levels.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING FEBRUARY 17:

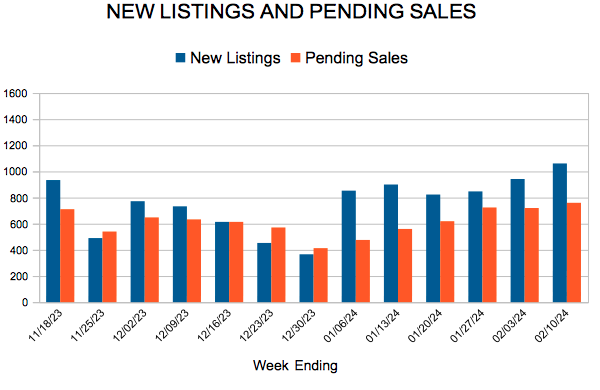

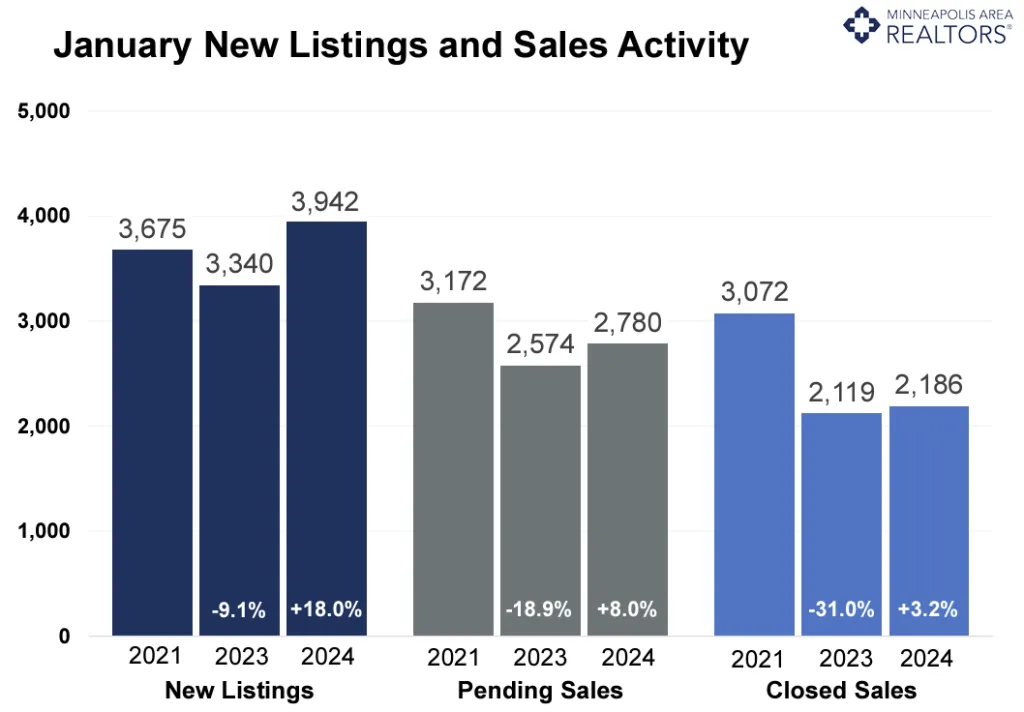

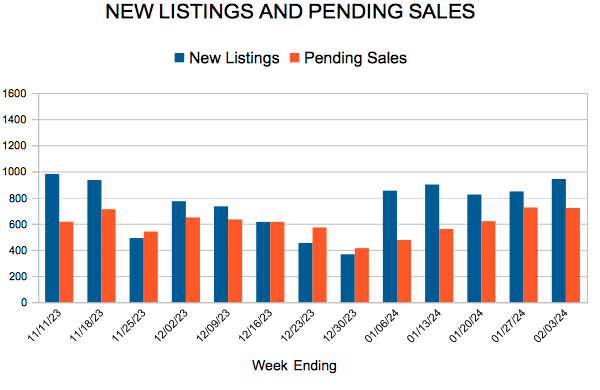

- New Listings increased 14.7% to 1,090

- Pending Sales increased 11.2% to 792

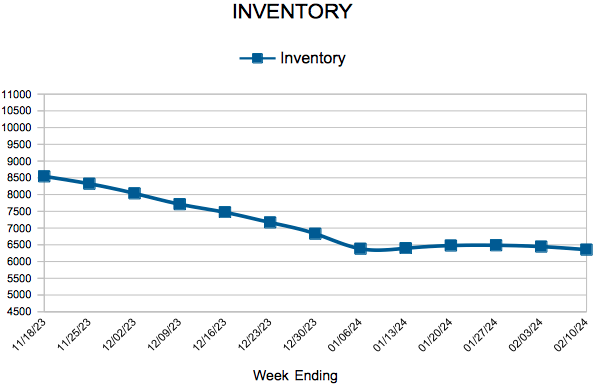

- Inventory increased 4.9% to 6,451

FOR THE MONTH OF JANUARY:

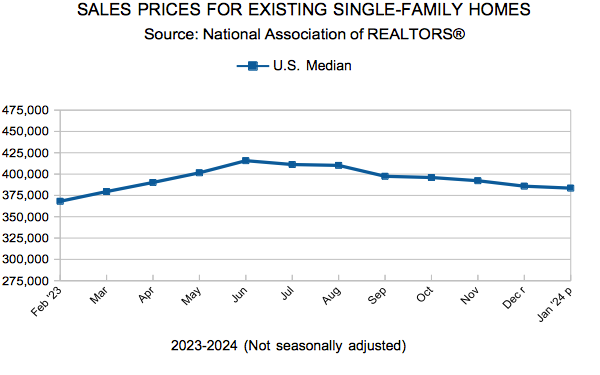

- Median Sales Price increased 3.1% to $352,500

- Days on Market decreased 8.2% to 56

- Percent of Original List Price Received increased 0.7% to 96.7%

- Months Supply of Homes For Sale increased 28.6% to 1.8

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.